Wisconsin Single Close Construction Loan: Your Path to a Smooth Building Experience

Building a home in Wisconsin is an exciting journey but can be somewhat winding when it has to do with dealing with finances. Traditional construction loans have many loans and closings, thereby upping the cost and factor of hassle. Fortunately, Single Close Construction Loans provide an efficient option with less headache. This blog will discuss the wonders of single-close construction loans, document their benefits, and explain how they work—with a guide to getting qualified.

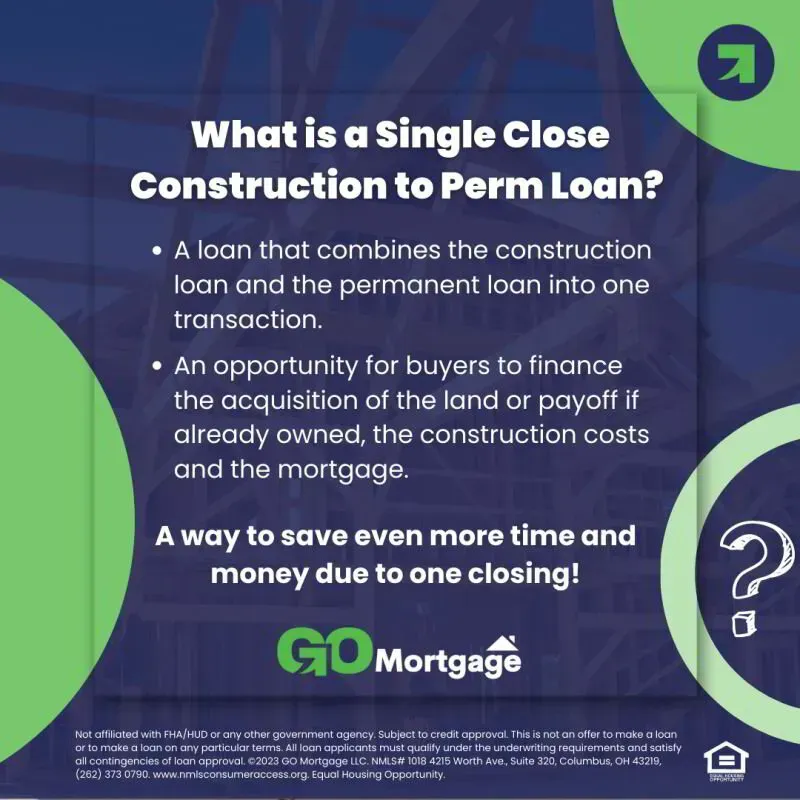

What is a Single Close Construction Loan?

Sometimes referred to as a one-time close construction loan, a single close construction loan combines construction financing in the same loan with permanent mortgage financing by applying just once, one approval, and one closing. Once the building phase is complete, the loan then automatically converts to a permanent mortgage.

Single Close Construction Loan Advantages Wisconsin

Easiness and Convenience

Single-close construction loans are more accessible and more convenient compared to multiple-close loans. There is the need for only one permanent loan approval, reducing paperwork and closing activities.

Combine Construction and Permanent Financing

Since this is construction and permanent financing under a single loan, you will save a lot on closing costs. Traditional construction loans require two sets of closing costs, but a single close loan requires you to pay just once.

Fixed Interest Rates

While not always the case, many single-close loans will be fixed rates rather than variable, where you lock in at a set amount at the beginning of the loan that you will have for the remaining life. In your budgeting, this can make your construction project more stable and predictable. If the borrower's situation calls for it, there is a feature for interest-only payments.

A single close construction loan will go a long way in helping to simplify and, hence, keep the process going without hiccups. Lenders often have their underwriting and closing departments set up with a team specializing in assisting to move the process along efficiently.

How Does a Single Close Construction Loan Work?

Application and Approval in Wisconsin

To receive a one-time close construction loan, you first apply to a lender that either provides funds for this loan directly or will sell the loan to a correspondent investor. The underwriter assesses your financial situation, credit history, and independent construction plans for your new dwelling. Disbursement is done in stages or "draws," which stop once the building process is completed. These drawdowns relate to all the construction processes, ensuring the project money is available in time. It is available only just in time, but it disburses only when work is accomplished.

Construction Phase

Lender often checks whether the work is being drawn, ascertaining that the project proceeds as projected and the money is spent appropriately. This type of checking ensures a seamless process of construction.

Permanent Mortgage Conversion

Construction is finished and the permanent mortgage starts automatically. You then make regular mortgage payments as you would for any home mortgage.

Single Close Construction Loan Eligibility and Requirements in Wisconsin

Good Credit Score in WI

A good or excellent level of credit will be required automatically if a buyer wishes to be considered for a single close construction loan by a lender. Good credit means high-paying power and reasonable terms. Talk to your licensed mortgage lender about the required credit score. Co-borrower's credit profile is of course used for the total loan.

Stable Income and Employment in WI

Evidence of stable income and employment status also forms a significant requirement for securing the loan. There will always be the wish by the lenders to have an assurance that you can manage to remit mortgage payments not only before the house is constructed but also after the construction period. You will also be required to provide your mail address, contact telephone, and e-mail address.

Choosing the Right Lender in Wisconsin

Not all lenders will do single close construction loans. Look for a proven construction loan lender: one that is going to offer some of the best and highly competitive fixed interest rates along with good terms throughout the entire life of your mortgage loan. The absolute best in customer service and support comes from having one mortgage lender. One possible lender of a mortgage is the Federal Housing Administration. If you are a veteran, you may also want to consider a VA loan. Because a VA is dependent on the conditions of the VA and veterans affairs, again, in the list of alternatives within the construction loan process may be an adjustable-rate mortgage; however, there come competitive mortgage terms available to a veteran in this type of loan. Indeed, there is a need for adequate research before choosing any of the programs.

Preparing Your Application in Wisconsin

To prepare your application, you will have to gather all your financial documents that relate to your current financial standing. This will involve tax returns, pay stubs, bank statements, or other documents showing your financial standing. The above documents will be handy to deduce your debt-to-income ratio.

Construction Plan Outline in WI

Make very detailed construction plans with your builder. This should be very comprehensive and meet the requirements that please the lender.

Working with a Builder in Wisconsin

Working with a Licensed Builder in WI:

Choose an experienced builder approved in single-close construction loans and licensed for the same. A builder should be in a position to offer you detailed plans as well as timelines that meet a lender's requirements. You must make a clean contract with your builder. This should outline all parts of the construction project, timelines, costs, and responsibilities. This contract will be an essential part of your loan application.

Navigating the Construction Phase in Wisconsin

Stay engaged with your project:

Throughout this phase of actual construction, regular inspections are a must. Stay in front of them, or if through your builder in Wisconsin, make the adjustments for the problems that might arise. Keep the channels of communication open for you, your builder, and your lender in the construction phase to avoid misunderstandings and to make sure that the project is on course.

Final Thoughts

A single close construction loan in Wisconsin can be an excellent option for building your dream home in Wisconsin. It simplifies the financing process, saves money, and offers peace of mind by combining the construction loan and mortgage into one seamless package. By understanding the benefits, requirements, and process, you can raise awareness, make informed decisions, and take the first step toward creating a home that perfectly suits your needs and lifestyle in WI.

If you’re considering building a home in Wisconsin, explore the benefits of a single close construction loan. Talk to knowledgeable mortgage loan officers; every home construction situation is a case-by-case basis. Learn more about your options and start your journey toward turning your dream home into a reality. Whether you’re looking for single closing, modular homes, short-term loans, shipping container homes, long-term financing, short-term financing, log cabin homes, single-family dwellings, or more, there is a solution for you.

If you’re looking for a construction to permanent loan in Wisconsin, Bob Fabian might be one of the best licensed lenders within the investor guidelines and loan originators. Bob connects consumers with a great interest rate and has consistently provided quality service. He will be with you every step of the way in the construction to permanent process for the proposed property. From residential loan types, multi-family units, single closing, accessory dwelling units, two-time close construction loans, construction to permanent loans, and a traditional mortgage, mortgage lender licensed Bob Fabian has got you covered.